Homeowners Vs Renters Insurance: Everything You Need to Know

As a homeowner or a renter, you must have insurance. Many unexpected events happen every day, and you do not want to be caught off guard. Maybe you or your family accidentally break a window, or one of your neighbors causes damage to the apartment you live in. Insurance will be there for you when such circumstances occur.

Homeowner’s and renter’s insurance does not cover the same types of damages, but there are a few similarities in their offering. Before settling on a type of coverage, be sure to know what differences they have.

- What is Homeowners Insurance?

- What is Renters Insurance?

- What Does The Homeowners Insurance Cover?

- What Is Not Covered By The Homeowners Insurance?

- What Does Renters Insurance Cover?

- What Cannot Be Covered By The Renters Cover?

- Cost Breakdown For Homeowners And Renters Insurance

- Factors Influencing Homeowners Insurance Policies

- Final Thoughts

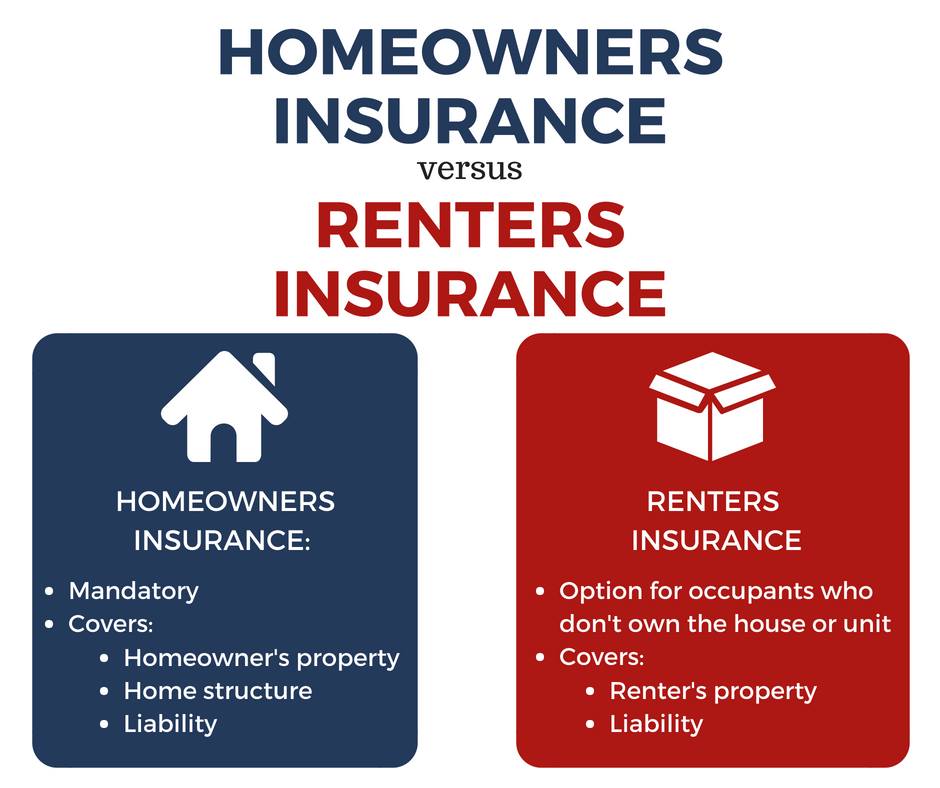

What is Homeowners Insurance?

Homeowner’s insurance is usually taken by the individual who owns the home. The insurance amount covers the replacement costs of the house and the personal property it holds at the time of an unforeseen event. These could be any furniture, electrical appliances, and accessories, among others.

The insurance also covers any injuries that happen within your property. In the case of a temporary relocation, your insurer may provide additional living expenses to assist you in settling.

Homeowners insurance is not a state requirement like car insurance. But if you are buying your home under a mortgage, your lender might need you to present homeowners insurance to approve your loan.

What is Renters Insurance?

Renter’s insurance covers people who are not owners of the property. It is provided for protecting personal belongings as they stay on the property or in the home. The landlord is only required to cover the building and any structure within the property.

Therefore, in case of theft and personal property damage, you need to have renters insurance. Renters’ insurance will refund all the replacement costs for lost or damaged items on the property.

You can also extend your insurance to cover special items such as artwork, jewelry, cameras, and other valued accessories.

What Does The Homeowners Insurance Cover?

- Dwelling Coverage

Perhaps the most significant factor that differentiates homeowner’s and renter’s insurance is the dwelling coverage. The coverage covers any structural damage to the home. It could be a smashed window, a broken door, and any other structure.

The coverage similarly extends to gardens, garages, and fences. Some damages may not be eligible for a payout. That is why there exist “covered events” and “named peril,” which should be directly paid by your insurance. They include natural phenomena such as hailstorms and winds, which are frequently occurring dangers.

- Personal Property

Homeowners’ coverage will also protect your belongings in your home. The object does not have to be within your home—the policy can also cover personal property stolen from your car.

In many cases, the price is bundled together with the dwelling coverage, and you only have to determine the amount of funds you will add or deduct from your policy.

- Personal Liability

In the case of someone getting an injury at your home, or if you get sued for personal damage within your home or property, the personal liability will come in handy to cover for you. The amount payable may vary depending on a few factors.

You may end up paying more if you have an aggressive pet that may cause harm to other people or if you have a few items and structures that pose dangers to individuals in your home.

- Medical Payments

The homeowner’s insurance also covers medical fees if someone gets injured on your property and needs medical assistance. Medical coverage does not hold you legally liable if someone gets hurt since it is on a no-fault basis.

- Additional Living Expenses

This is also known as loss of use coverage, and it provides you with extra income to protect you from financial hardship while living outside your home, whether rental or owned. These expenses will be covered if your home has been rendered uninhabitable in the event of peril. You could be covered for your hotel fees for a specified limit as stated by your insurance provider.

What Is Not Covered By The Homeowners Insurance?

Significant events such as earthquakes and floods usually cause intense damage, covered under a different policy. If you live in areas prone to flooding or earthquakes, you might need additional cost coverage besides the dwelling coverage. This is why you need to know ways to lower homeowners insurance costs.

It is also important to note that homeowners insurance does not cover damages resulting from negligence damages that would be avoided if occasional maintenance was considered.

In the case of power failure or government-instructed demolitions, the policy will not cover such.

What Does Renters Insurance Cover?

- Personal Property

The main reason for having renters insurance is to cover your personal property—home equipment, electronics, and clothing, among other items. Before taking a policy, you need to inventory your personal belongings and determine what replacements would cost. The amount you come up with will be your limit.

You may choose between “replacement cost” and “cash-value” and how much cash your belongings are valued at. Replacement costs mean that you will pay more premium when your items get damaged. You can pay an extra $20 or $50 every year.

Since you have auto insurance, your car will not be included in the personal property policy. Only items lost in your vehicle are eligible for coverage even if the vehicle is away from your property.

Read Also: How to save big on your car insurance

- Personal Liability

This coverage comes into play if someone gets injured while on your premises. It is no different from the homeowner’s coverage. If damages to the building as an accident, you can be protected from your landlord’s lawsuit.

What Cannot Be Covered By The Renters Cover?

Renters’ insurance does not cover dwelling since renters are not directly responsible for the building they live in. in the case of structural damages, renters do not have to pay for anything.

Renter’s personal property reimbursements are limited to the “named perils” or “covered events” listed by the insurer.

The policy will only cover the person who pays for it, either married couples or families. If you live with roommates, each of you will have to get separate insurance policies if they need them.