How to Consolidate Debt: Debt Consolidation Loan

Unless you are swimming in loads of cash, debt is inevitable, hence the need to learn how to consolidate debt. When used correctly, debt can help you amass wealth, but in the wrong hands, you will be digging yourself into a hole that is quite difficult to get out of without financial discipline.

In an era where getting credit cards is easy, people are tempted to spend more than their earnings with the promise of credit card rewards, such as cash-backs or traveling miles.

We forget that credit cards have the highest interest rates compared to other loans, meaning that the amount you owe will balloon out of control quickly. When you have several loans and are looking for an easy way to pay them quickly, you can consider combining them into one.

This will make it easy to track, and you will be able to make more than the minimum amount of payment.

The majority of consolidation strategies give you a chance to enjoy a lower interest rate, allowing you to save on the overall interest paid, thus paying off your debt faster.

This article presents you with different ways to consolidate your loans but before that, let’s understand debt consolidation and its merits and demerits.

What Is a Debt Consolidation Loan?

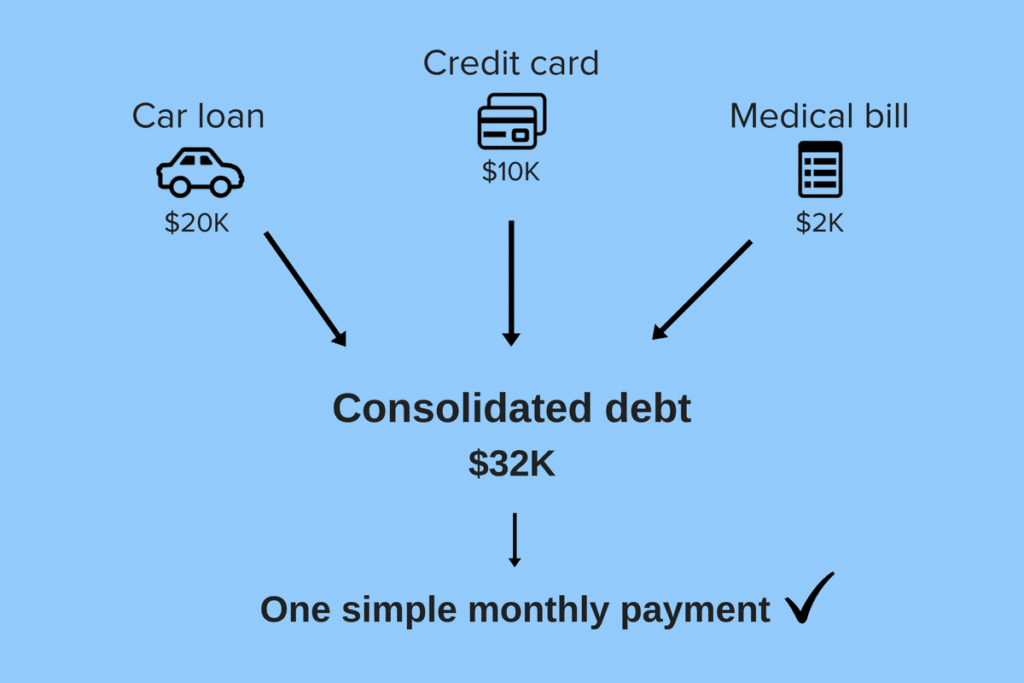

Debt consolidation is a loan repayment strategy that requires combining several loans, especially high-interest rate loans such as credit card debts, into a single payment.

This often is done by a bank, and it is only an option if you get a lower interest rate which will help you reduce your total debt, enabling you to pay it off faster.

However, before you consolidate your debts, ensure that you have a good credit score and a good history of paying bills. Otherwise, you will not be approved for a debt consolidation loan, or you get a higher interest rate, which would be worth consolidating your debts.

You can also consolidate your debt without taking out a loan and enroll in a debt management plan. This is a service offered by non-profit credit counseling agencies that work with your lender to negotiate lower interest rates, which equals lower monthly payments.

These agencies include InCharge Debt Solutions, and the good thing is they do not use your credit score.

Read Also: How to fix your bad credit score

Benefits Of Debt Consolidation Loan

- Lower Interest Rates

The main reason why people choose to consolidate their debts is to enjoy lower interest rates, especially if you have a superb credit score. Thus, people with high-interest loans prefer to consolidate, especially if the loan term is not long. Therefore, shop around and settle on the lenders that offer a personal loan prequalification process.

- Improves your credit score

While taking out a new loan lowers your credit score and increases credit utilization because of the hard credit inquiry, debt consolidation helps improve your credit score. You may be wondering it’s also a loan; how can it improve the credit score?

Debt consolidation involves paying off your open credit lines, thus reducing your credit utilization, which is supposed to be under 30%. And your credit score improves as you continue paying off your loan.

- Less stressful

Since you combine all your debts into a single loan, debt consolidation removes the stress of managing monthly payments for several loans and tracking them.

Therefore, you do not need to worry about missing a payment because consolidation reduces the chances of forgetting to make your monthly deposit. It’s even better if you automate the payment to coincide with your pay date.

It also helps you set a date when you intend to finish paying off your loan.

- Faster loan repayment

When you consolidate your debts, you have a chance of getting a lower APR, meaning that your overall interest rate will also be lower. This enables you to pay off your loan faster since you can also make extra payments, allowing you to save even more on interest. Note that debt consolidation leads to extended loans, which means you will have to be consistent in paying off your debt to clear it faster.

- Reduces monthly payment

When you consolidate your debts, your monthly payments are reduced because your payments are spread out over a new duration, which is usually extended. Although it ensures that you will not struggle with the monthly payments, it also means that you might end up paying more over the life of the loan, even with the low-interest rate.

Cons of Debt Consolidation Loans

Every good thing has its downside, and debt consolidation is no exemption. Discussed below are some of the cons associated with this debt repayment strategy.

- Additional costs

You must understand that you will be required to pay some fees before you consolidate your loan. They include:

- Origination fees

- Closing costs

- Balance transfers

- Annual fees

So make sure that you ask your lender about all the fees involved and if there are penalties for paying off your loan earlier or making prepayments. This will allow you to determine whether debt consolidation is worth it.

- Higher interest rate

Your debt consolidation may be available at a higher interest rate than what you are currently paying. This could be attributed to a low credit score and poor credit report.

Another reason your interest may be high is spreading out your loan for a long duration, where your overall interest ends up being more.

So before consolidating your debts, evaluate your immediate need and long-term goals and ensure that you choose the ideal method.

- Missing payments

If you miss any of your monthly payments, you may damage your credit score and set yourself back further because of the added late payment fee.

So ensure that you make miss payments by more than 30 days because the information will be remitted to the credit bureau, thus damaging your credit score.

To minimize your chances of missing payments, automate your monthly payments and ensure that they coincide with your pay date so that your account will always have money.

- It does not get rid of the underlying issues

Debt consolidation will help you pay off your loans but set up an emergency fund if you do not address why you are in debt. You will be back in a debt rabbit hole very soon.

To maintain healthy spending habits, track your spending, create a budget and stick to it. After you are through paying off your debt, identify your next goal, and start on it.

You can start saving and investing for retirement and make sure that the money works for you by investing.

Read Also: How to create a budget